Remote Work and Urban Development After COVID

Remote work changed the map. Not everywhere, and not in the same way, but enough that planners, developers, homeowners, and city officials can no longer treat it as a temporary pandemic habit. The office did not disappear. Cities did not collapse. Rural towns did not all become boomtowns. The more interesting story is messier: people gained more freedom to separate where they work from where they live, and that freedom pushed housing demand, daytime spending, and development pressure into new places.

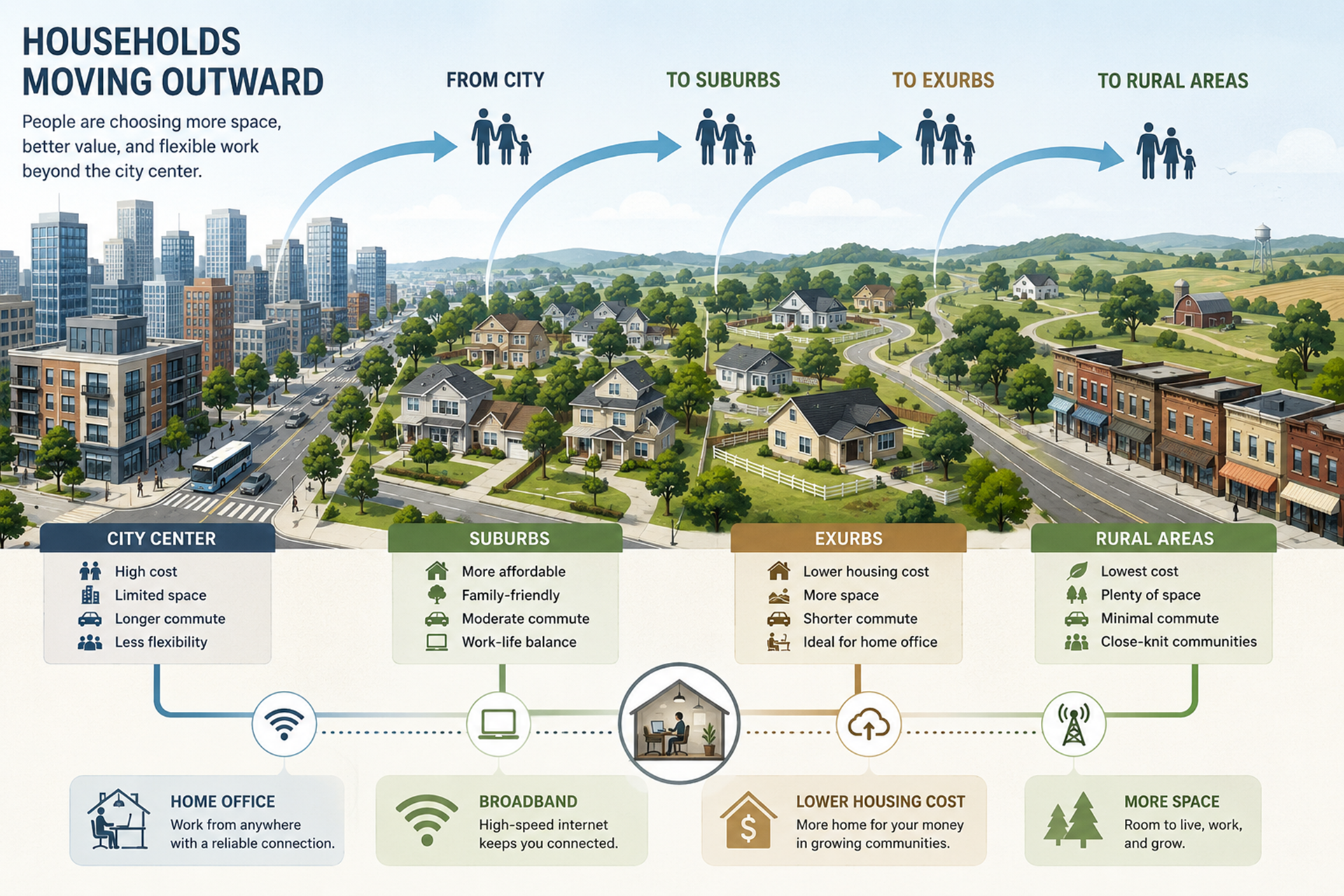

The clearest shift came from workers who no longer needed to commute five days a week. Some moved farther from expensive urban cores. Others stayed in the same metro area but chose bigger homes, quieter suburbs, or exurban towns where a home office and a yard were possible. Census data shows that the share of U.S. workers usually working from home remained more than twice its pre-COVID level in 2023: 13.8% in 2023 versus 5.7% in 2019 [1].

The result is not simply “cities lost, suburbs won.” Remote work has produced a new development pattern: office-heavy downtowns are being pushed to become more mixed-use, suburbs are absorbing more housing and retail demand, and rural or small-town communities are navigating the benefits and strain of newcomers. The big question is no longer whether remote work matters. It is how communities should build around it.

Remote Work Became a Land-Use Force

Remote work used to be discussed mostly as an employee perk. After COVID, it became a land-use force. When millions of people stopped commuting daily, cities lost not only office attendance but also the predictable weekday movement that supported transit systems, lunch counters, dry cleaners, downtown gyms, and office-adjacent retail. The U.S. Census Bureau described how daytime populations in traditional job centers fell sharply in 2020, affecting commuter-driven spending and commercial real estate demand [2].

This matters because cities are built around routines. A downtown designed for Monday-through-Friday office workers depends on elevators filling at 8:30 a.m., cafés turning over tables at lunch, trains and buses carrying peak-hour riders, and office landlords renewing leases. When hybrid work reduces those routines, the built environment does not immediately adjust. Buildings remain, leases roll over slowly, transit budgets lag, and restaurants can’t instantly move to where customers now spend their weekdays.

The persistence of remote work also differs by measurement. Census ACS data captures workers who “usually” work from home, while the BLS American Time Use Survey measures whether employed people spent time working at home on days they worked. In 2024, BLS reported that 33% of employed people spent some time working at home on days worked, close to 35% in 2023 [3]. That does not mean one-third of workers are fully remote. It means home has become part of the normal work geography.

The best development lens, then, is not “remote versus office.” It is how many days per week people need proximity to an office. A worker commuting one day a week can live much farther out than someone commuting five days a week. That small schedule change can reshape housing demand across an entire metro region.

Why Suburbs, Exurbs, and Rural Areas Gained Attention

When work becomes less tied to downtown, the home itself becomes more valuable as a workspace. That changes what buyers look for. A spare bedroom, a finished basement, a quiet office nook, reliable broadband, a larger kitchen, and outdoor space become more important. For many households, those features are easier to find outside dense urban cores.

The Philadelphia Fed summarizes the mechanism clearly: work from home increases demand for homes that can also function as office space, and it encourages households to move toward lower-cost or higher-amenity areas [4]. That does not mean remote work caused every move to the suburbs. Housing affordability, family formation, school preferences, safety perceptions, climate, taxes, and aging also matter. Remote work simply lowered the penalty for living farther from an office.

Census population estimates released in 2026 show that growth since 2020 often occurred on the outer edges of major metro areas, though not uniformly across every city [5]. Dallas-Fort Worth, New York, Minneapolis-St. Paul, and Seattle-Tacoma each showed different patterns, but the Census Bureau still described growth farther from metro centers as a dominant trend in the selected metros [5]. That is exactly the kind of uneven pattern remote work tends to create: strong effects where jobs are remote-capable, housing is constrained, and farther-out communities have room to build.

Rural areas saw a related but more selective effect. Scenic towns, lower-cost counties, and communities near regional metros attracted remote workers seeking space and affordability. But rural growth was not automatic. Places without broadband, healthcare access, housing supply, or transportation links often struggled to capture the shift. Remote work may free workers from the office, but it does not free them from basic infrastructure.

For communities receiving remote workers, the upside can be meaningful. New residents bring income, property demand, local spending, and sometimes entrepreneurship. They may support restaurants, contractors, fitness studios, childcare providers, and home-improvement businesses. But the same inflow can raise prices faster than local wages, especially in towns where housing supply is thin.

The Economic Impact on Downtowns and Office Districts

Downtowns were not built only for residents. Many were built for commuters. Remote and hybrid work hit that model by reducing the number of weekday office workers buying coffee, taking transit, eating lunch, shopping after work, and filling office towers. The Census Bureau noted that fewer workers in job hubs meant fewer shoppers and diners for small businesses in those places [2].

The strongest pressure falls on office-heavy districts with limited housing, weak evening activity, and older office buildings. McKinsey’s research on “superstar” cities found that office attendance stabilized about 30% below pre-pandemic norms, and that demand for office space in a median studied city could be 13% lower in 2030 than in 2019 under a moderate scenario [6]. The same report found foot traffic near metropolitan stores remained 10% to 20% below pre-pandemic levels, with office-dense urban cores facing deeper retail pressure [6].

That weakness can ripple through city budgets. Office buildings generate commercial property taxes. Downtown workers generate sales taxes, transit fares, parking revenue, and business activity. Pew’s 2026 look at Atlanta, Boston, Dallas, Denver, and Milwaukee found that these cities had not fallen into a “doom loop,” but it also warned that reduced office values may take time to appear in tax collections [7]. In plain English: the full fiscal impact can arrive slowly, after leases reset, properties are reassessed, and owners challenge valuations.

Still, downtowns are not doomed. The places adapting fastest are treating remote work as a design problem, not just an economic shock. They are pushing office-to-residential conversions where feasible, adding housing near transit, activating ground floors, improving public spaces, and trying to make downtown attractive even when workers are not required to be there five days a week.

Housing Prices, Construction, and the New Space Premium

Remote work did not create America’s housing shortage. It exposed and intensified it. The most important housing effect was demand for more space: not necessarily luxury, but functional space. Households wanted a desk behind a door, a yard for kids, a less punishing commute, or the ability to live near family while keeping a metro-area salary.

NBER research by John Mondragon and Johannes Wieland found that pandemic-induced remote work caused a large increase in housing demand and accounted for at least half of recent aggregate U.S. house price growth during the studied period [8]. The same research estimated that one additional percentage point of remote work during the pandemic corresponded to an additional 0.93 percentage point increase in house price growth from December 2019 to November 2021, after controlling for net migration [8].

The same study also found that remote work was associated with rent growth and increased building permit issuance [8]. That matters for urban development because housing demand does not only move people; it moves capital. Developers follow demand to exurbs, edge suburbs, second-home markets, and regional towns. Builders add subdivisions, accessory dwelling units, townhomes, and single-family rentals where zoning, land availability, and infrastructure allow.

But new construction creates a second-order problem: infrastructure strain. A fast-growing suburb may need road widening, water systems, schools, emergency services, parks, and stormwater planning long before the tax base fully catches up. A rural town that gains remote workers may benefit from higher home values, but local renters and first-time buyers may be priced out. The economic gain is real. The affordability pressure is real too.

The “space premium” also changes housing design. Builders now market flex rooms, pocket offices, detached studios, sound-insulated workspaces, larger kitchens, and better wired homes. Broadband becomes as important as a garage. A home without reliable internet is no longer merely inconvenient; for remote workers, it can be economically unusable.

What Local Governments Need to Plan For

Remote work forces local governments to plan for a more distributed economy. Cities that lost office foot traffic cannot simply wait for the old commuter pattern to return. Suburbs and rural communities that gained residents cannot assume growth will pay for itself. Both sides need more flexible land-use policy.

For central cities, the priority is converting single-purpose office districts into neighborhoods people use all week. That means housing, schools, childcare, grocery stores, entertainment, parks, and transit service that works outside peak commute hours. Pew found that office-to-residential conversions are a key strategy for cities trying to bring underused buildings back into productive use and address housing shortages [7].

Conversions are not easy. Many office buildings have deep floor plates, limited plumbing stacks, awkward window access, and financing problems. Cities may need tax incentives, faster permitting, zoning reforms, and public-private partnerships. Some older Class B and Class C buildings will not convert cleanly. In those cases, reuse may involve education, labs, hotels, coworking, civic facilities, or demolition and rebuild.

For suburbs and rural communities, the issue is managed growth. More residents can support local business and expand the tax base, but scattered development can increase traffic, infrastructure costs, and environmental pressure. Communities should ask practical questions before approving growth: Is broadband available? Can local roads handle the volume? Are schools prepared? Is there enough rental housing for service workers? Are new homes being built in flood, fire, or drought-prone areas?

Brookings warned that pandemic-era migration sometimes placed more people in regions exposed to climate risks such as wildfire, drought, and hurricanes [9]. That does not mean every move away from a city is risky. It does mean local planning should not treat affordability today as the only variable. A remote worker moving to a lower-cost area still needs insurance, resilient infrastructure, and safe land-use decisions.

Who Benefits, Who Gets Squeezed, and What Comes Next

Remote work created winners, but not evenly. High-income, college-educated workers were more likely to work from home than many service, manufacturing, retail, and transportation workers. Census data shows home-based workers tend to be older, more likely to be White, and less likely to be in poverty than commuters [1]. BLS also reported that in 2024, workers with a bachelor’s degree or higher were much more likely to work at home on days worked than workers with a high school diploma and no college [3].

That inequality matters for urban development. Remote workers can bring higher outside incomes into lower-cost towns, which can be positive for local spending. But if local wages do not rise with housing prices, teachers, restaurant staff, nurses, municipal workers, and young families may struggle to stay. The development story therefore includes not only migration but class tension.

There are also benefits that are easy to miss. Reduced commuting can lower household transportation costs and give workers more time. Less peak-hour traffic can reduce emissions and congestion. Smaller towns can attract skilled residents without recruiting an entire corporate office. A region with good broadband and quality-of-life amenities may now compete for talent in ways that were previously impossible.

The next phase, through 2026 and beyond, will likely be hybrid rather than fully remote. That still changes development. Even two remote days per week can reduce downtown spending, make longer commutes tolerable, and shift demand toward homes that support office work. Cities and towns that plan around hybrid reality—not a full office return or a total remote future—will have the better odds.

A Better Way to Think About Remote Work and Place

The old model treated work as a place people went. The newer model treats work as an activity that may happen at home, in an office, in a coworking space, or across all three. That single change alters what households value, where developers build, how downtowns function, and how local governments collect revenue.

Remote work did not end urban development. It widened the map. It made the outer edges of metros more attractive, gave some rural and suburban communities a new economic opening, and forced downtowns to become more than office storage. The communities that handle this well will not be the ones that simply chase growth. They will be the ones that pair growth with housing supply, infrastructure, broadband, mixed-use design, climate awareness, and realistic fiscal planning.

The practical question for readers is simple: look at your own town or city and ask what weekday life now looks like. Where are people spending money at noon? Where are homes being built? Which streets are busier than they used to be? Which office blocks feel emptier? Those clues reveal how remote work is reshaping place—not as a theory, but as a pattern already visible on the ground.

References

- U.S. Census Bureau. “Socioeconomic Inequalities Between Remote Workers and Commuters,” January 16, 2025.

- U.S. Census Bureau. “Remote Work During the Pandemic Shifted Daytime Population of Cities,” February 21, 2023.

- U.S. Bureau of Labor Statistics. “American Time Use Survey — 2024 Results,” June 26, 2025.

- Federal Reserve Bank of Philadelphia. “The Geographic and Economic Implications of Working From Home.”

- U.S. Census Bureau. “Movin’ Out: More Growth on Outer Edges of Major Cities,” May 14, 2026.

- McKinsey Global Institute. “Empty Spaces and Hybrid Places: The Pandemic’s Lasting Impact on Real Estate,” July 13, 2023.

- The Pew Charitable Trusts. “The Remote Work Challenge: Lessons From 5 Cities,” May 2026.

- National Bureau of Economic Research. “Pandemic-Induced Remote Work and Rising House Prices,” July 2022.

- Brookings Institution. “How the Pandemic Changed—and Didn’t Change—Where Americans Are Moving,” September 6, 2024.